LINK Should Be Missing From Cash Access Decision Making

Posted on: 13/10/2025

In December 2017, LINK Scheme Ltd created a “World First” when announcing that there were too many ATMs in the UK.

LINK - ultimately beholding to the big banks - stated that this was costing those banks “a fortune”.

Leicester Town Centre was highlighted as the location most over supplied with ATMs.

LINK said they would reduce payments to ATM operators so that major city centres would have fewer ATMs, which would allow LINK to ensure smaller communities would retain their ATM services.

This messaging from LINK was nonsense.

Firstly, having those ATMs in Leicester was not costing banks “a fortune”, for the very good reason that banks are NOT paying per ATM; they are paying per transaction.

So 20,000 LINK cash withdrawals made via 65 ATMs costs banks exactly the same as 20,000 such withdrawals via 40 ATMs.

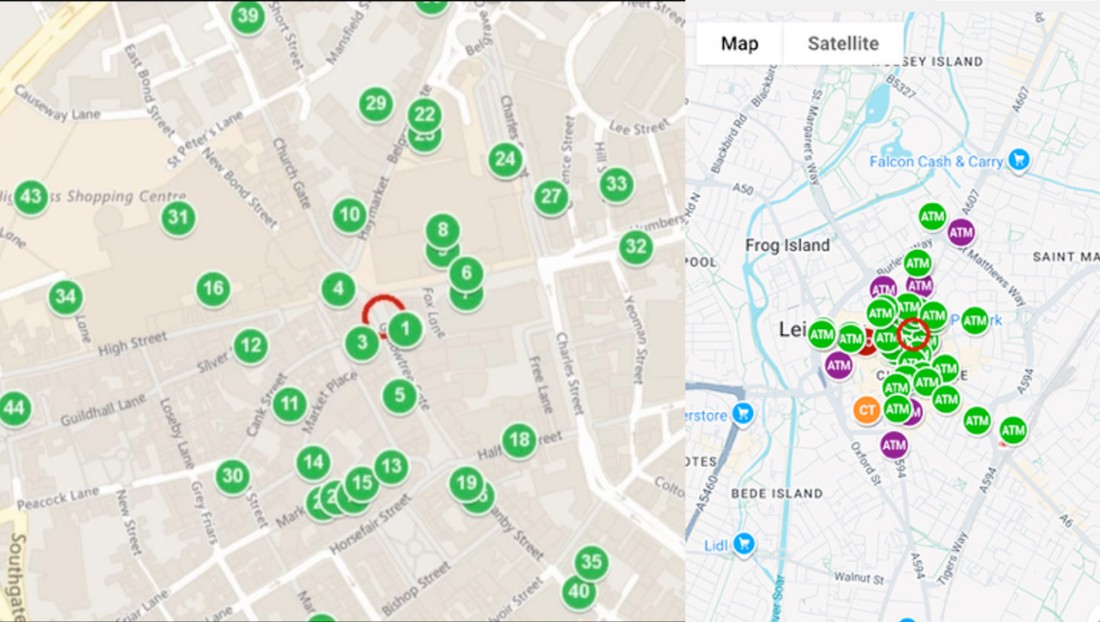

Secondly, have a look at the two images above.

On the left hand side is the map of Leicester Town Centre ATMs in 2017 - the image used by LINK when they made their “too many ATMs” claim.

On the right hand side is the map of Leicester City Centre last Friday.

Notice how many ATMs are still there.

Since LINK weaponised payments to ATM operators, the UK has lost more than 20,000 free-to-use ATMs - getting on for 40% of the entire LINK network.

But the main reduction in numbers has NOT been in major city centres such as Leicester. The main losses have been in smaller communities and particularly those with less than 70000 residents.

Leatherhead is a particularly striking example.

When LINK made their announcement in December 2017, Leatherhead had 15+ free-to-use ATMs - by 2023 this had been reduced to only ONE.

Leatherhead is perhaps particularly startling - but there are around 2000 communities in the UK with between 70000 and 4000 residents, most of which have lost most/all bank branches and multiple ATMs.

In such smaller communities, where only one or, if they are lucky, two ATMs are now left, it may now be several minutes walk to the nearest ATM.

This plainly discourages cash use.

Another factor is that, with only one or two ATMs left, a couple of faults or cash outs can leave a community without any convenient cash access for days

Make no mistake.

The weaponising of payments to ATM operators was aimed at reducing ATM numbers in smaller communities and, in doing so, quite deliberately reduce convenient access to cash and, ultimately, cash use by the British public.

LINKs manoeuvres were also intended to support the bank branch closure programme, by ensuring it was uneconomic for any ATM operator to replace the ATMs being ripped out of defunct branches.

All of this should come as no surprise, since a stated objective of LINK is “to support the UK's orderly transition from cash to digital payments.”

Since 40 million British adults do not agree that cash is in need of a digital solution or transition, it’s clear LINKs objective is NOT in the Public Interest.

It follows that LINK should NOT be deciding the future of cash in the UK, either nationally or at community level.

All rights reserved. No part of this website can be reproduced, shared or transmitted in any form or by any means without the prior permission of the copyright owner.